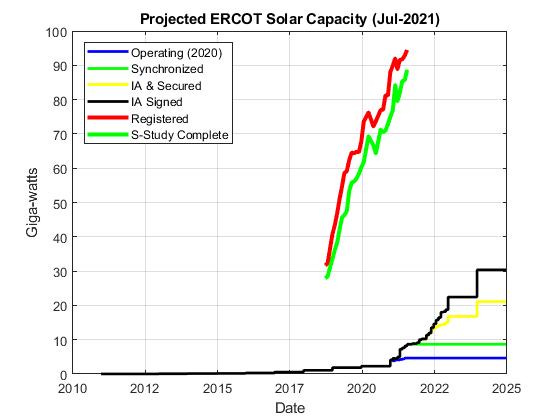

In our recent post1 the ERCOT new solar and wind project projections were discussed. For solar, over 20 GW of peak capacity is expected by the end of 2023 and by then, wind nameplate capacity should be about 39 GW. The solar growth has been and is exponential. Wind’s growth seems to be turning over, but it isn’t zero yet.

Even more stunning is the amount of solar in the early stages of development with over 90 GW of projects in various stages of development. Most of this is in the early stages with the bulk of it having completed the screening study and are currently in the full interconnect study. (It can’t be easy to fully gauge the effect of a new plant with so much capacity under consideration.)

Surely it makes no sense to install 90 GW of supply in an ISO whose peak load is in the mid 70-GW range, does it? With the amount of solar (and wind) power available having temporal dispatch uncertainty, the answer fully depends upon the amount of electric energy storage available to capture the variable power. Batteries in theory have the ability to take an uncertain supply and turn it into a highly certain one. If it can do that economically, then, as the expression goes, it’s a whole new ball game.

Battery Pipeline

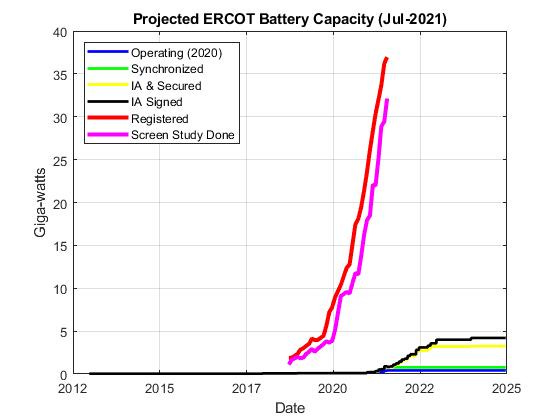

Here is the plot of the projected ERCOT battery deployment. Currently the amount of synchronized capacity stands at 0.354 GW, a drop in the bucket. The amount that has progressed to the point of having an Interconnection Agreement and that has a projected commercial operation date prior to 2024 is 4.2 GW—that’s a number worth noticing, and this capacity could have an effect on the edges of the pricing distributions. But, as with the solar project pipeline, the early stage battery pipeline is even more striking with over 35 GW of capacity under different stages of development.

With 35 GW of deliverability from storage, all of a sudden 100 GW of solar capacity doesn’t seem so crazy, if the power can be captured when the sun is shining or the wind is blowing and then dispatched later when the market signals the need. A reasonable number for both wind and solar time-averaged dispatch to nameplate (i.e. peak) capacity is around 35%. (People will quibble with that number, and I won’t argue with you at the few percent level, but let’s keep the discussion simple.) So, 100 GW of nameplate solar in Texas, if storable and dispatch-able, is equivalent to about 35 GW of callable summer time supply—about the amount of battery capacity being considered. That is probably not a coincidence.

Dispatch-ability

There is so much to consider when looking at batteries such as install cost and ROI which is being glossed over in this note. To get it right one needs to understand the nature of batteries including their charging and discharging rates, their cyclability and lifetimes under different operating conditions and etc. Then there are the transmission constraints and real-time versus day-ahead pricing. The subsidy details are also important—especially for solar. Most of that we skip for now. Here we consider only two questions: (1) deliverability, and (2) duration.

In the swing seasons with the present installed renewable assets, ERCOT already sees prices going to zero or negative when supply is more than needed and/or supply gets stranded by transmission constraints. To circumvent the transmission problems, it helps to have storage near the generation assets. ERCOT in their Battery report includes the fraction of how much is co-located with which type of assets. Most of the projected battery supply is listed as Stand-Alone, but over the past year, the pipeline is becoming more populated by storage projects co-located with solar or wind as shown in the following ERCOT-produced graphic. With co-location, deliverability issues are still present but reduced.

The other issue is the duration of the energy storage. The number associated with battery storage, or for any asset for that matter, is the amount of power that can be dispatched. For batteries an important question is “For how long can the battery supply the stored electricity?” Fortunately, ERCOT provides some transparency on that number too. The next graphic shows the distribution of the battery duration for those currently installed and those still in planning. It looks like the bulk of the supply is currently only short-duration at their quoted capacity. In other words, batteries listed at 100 MW can supply that amount of power for about 1 hour on average.

An important point of fact however is that the battery doesn’t have to run down so quickly. A 100 MW-1 hour rated battery could also serve 20 MW for 5 hours if need be.

There are many parameters here. Could 100 GW of solar capacity at peak sun supply say, 30 GW now (constraint issues?) and then store the 70 GW for later? If so, assuming 12 hours of “later” you get about 5 GW (after losses) of dispatchable power in the off-hours. That would not be irrelevant.

Summary

Once the battery pipeline is presented, the crazy-looking solar pipeline numbers come more into focus and don’t look quite so crazy. Bold is a better word. The game is moving towards making solar and wind assets look similar to callable assets like gas-combined cycle plants. It remains to be seen whether or not this pipeline can be implemented economically and without too many hiccups, and it isn’t at all clear with the present economics that battery storage can transform a solar plant a 24/7 plant. It is a game-changer if it can, and its development must be watched.